2026 Hurricane Season Money Checklist: Flood Insurance, Deductibles, Cash, and Documents

Hurricane season is not only a weather story.

If you own a home, rent near a flood-prone area, keep a car in a low-lying neighborhood, have a basement, care for older relatives, or have pets, hurricane season is also a household cash-flow test. Wind damage, flooding, power outages, delayed transfers, missing claim documents, and temporary relocation can all turn an otherwise stable budget into a scramble.

NOAA's 2026 Atlantic hurricane outlook calls for a higher chance of a below-normal season, but that does not mean zero risk. NOAA notes that the Atlantic hurricane season runs from June 1 through November 30, and even a quieter season can still produce damaging storms. Source: NOAA 2026 Atlantic hurricane outlook.

This guide is not trying to predict which storm will hit where. It asks a more practical question: if a storm watch appears this week, are your insurance, cash, documents, and records ready?

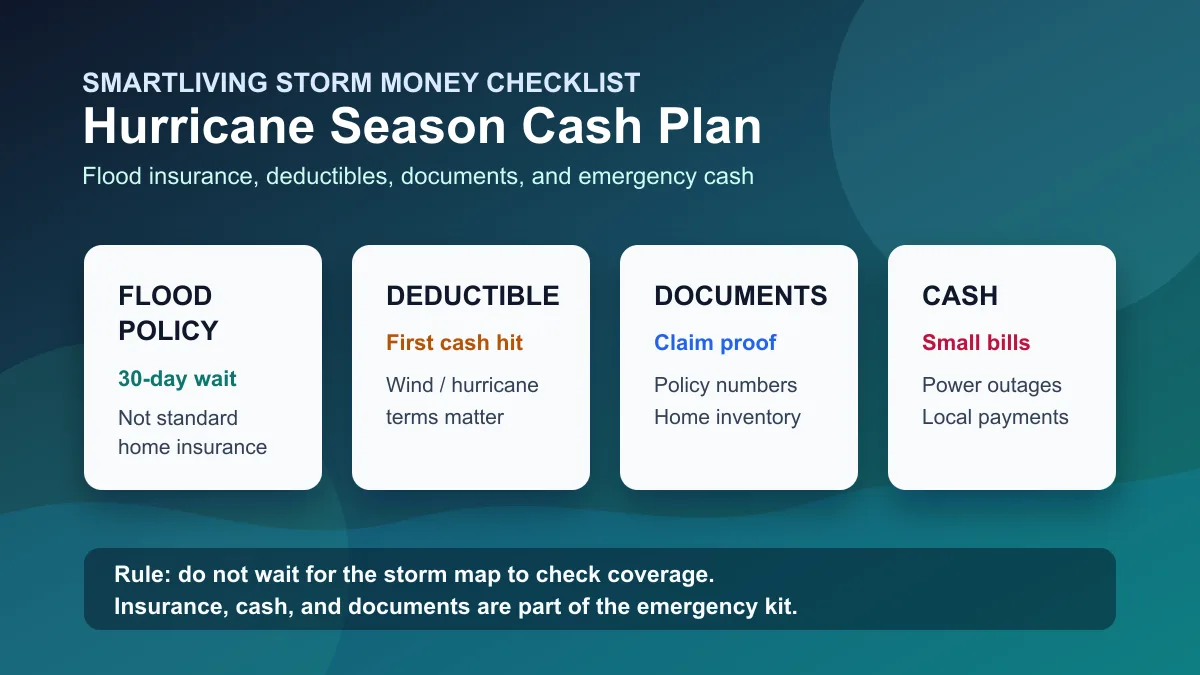

Start Here: Homeowners Insurance Usually Does Not Cover Flood Damage

Many homeowners assume that because they have homeowners insurance, they are covered for storm damage. That assumption can be expensive.

FEMA and FloodSmart both explain that most homeowners insurance does not cover flood damage; flood insurance is a separate policy. Sources: FEMA Flood Insurance and FloodSmart: Buy a Policy.

That distinction should change your preparation order. Wind damage to a roof, a tree falling on the home, or rain entering through a storm-created opening may belong in a homeowners-insurance discussion. Storm surge, surface water, river flooding, and basement flooding may fall into flood-insurance territory. Exact coverage depends on your policy, but "I have home insurance" should not be translated into "I have flood protection."

If your homeowners insurance renewal or escrow statement recently jumped, pair this with the SmartLiving guide here: Homeowners Insurance Premium Audit Guide 2026. Before hurricane season, the question is not only whether the premium rose. It is where the coverage gap sits.

Step 1: Check Flood Insurance Before a Named Storm Is on the Map

FloodSmart says NFIP flood insurance coverage generally begins 30 days after the purchase date, with limited exceptions such as policies connected to making, increasing, extending, or renewing a mortgage, renewal changes, and certain newly designated high-risk flood zones. Source: FloodSmart: waiting period.

That is why waiting until a storm is already being tracked can be too late. Insurance is not an umbrella you buy after the rain starts. It is a protection layer that usually has to be in place before the event.

Start by checking three things:

- Whether your address is in or near a FEMA flood-risk area.

- Whether your homeowners policy excludes flood damage.

- Whether your mortgage lender requires flood insurance, and whether the policy has remained active.

Condo owners, co-op owners, renters, and landlords should not skip this step. You need to understand what the building policy, HOA master policy, personal contents coverage, and renters policy each cover.

Step 2: Treat Insurance Documents Like Cash-Flow Tools

One of the worst post-storm problems is having insurance but not knowing the policy number, deductible, coverage limit, claim phone number, or portal login.

Ready.gov recommends building an emergency kit and keeping important documents available. Source: Ready.gov Build A Kit. From a household finance angle, documents are not about being tidy. They are about being able to prove who you are, what you own, what is insured, and whom to call when the power is out or you have evacuated.

Create a simple storm folder, both digital and paper:

- homeowners insurance declarations page

- flood insurance policy

- auto insurance

- mortgage servicer information

- property tax and escrow statement

- deed or closing statement

- copies of passports, driver's licenses, green cards, or other IDs

- health insurance cards and prescription list

- family and pet information

- insurance claim phone numbers and app login instructions

Store digital copies in encrypted cloud storage if possible, and keep paper copies in a waterproof bag. Do not keep the only copy on a home computer that could flood with the house.

Step 3: Keep Small Bills, Not a Large Cash Hoard

After a hurricane or flood, the problem may not be that you have no money. It may be that your money is temporarily hard to use. Power outages, weak cell service, card-reader failures, ATM lines, and local merchant disruption can make small cash useful.

This does not mean storing large amounts of cash at home. That creates theft and loss risk. A more practical range is enough for two or three days of essential local spending: gas, parking, simple food, medicine, local transport, or small repair supplies.

For many households, $100 to $300 in small bills is more useful than a single stack of $100 notes. The goal is not investment optimization. It is keeping the household functioning when the payment system is temporarily clunky.

Step 4: Read the Deductible Before You Read the Premium

Many people shop insurance by premium. Before hurricane season, read the deductible.

Your policy may have a normal deductible and a separate wind or hurricane deductible. The hurricane deductible may be a percentage of the dwelling coverage limit, not a fixed dollar number. If the home is insured for $500,000 and the hurricane deductible is 2%, the first cash hit could be $10,000.

That is why insurance and emergency funds belong in the same conversation. If your deductible is much larger than your available cash, the policy may still be valuable, but you need to know how much you must absorb before the policy meaningfully helps.

Ask these questions:

- What is the hurricane or wind deductible?

- Is flood completely excluded?

- Is basement property covered?

- How does loss-of-use or temporary living expense coverage work?

- Are tree removal, roof damage, water backup, or sump failure subject to separate limits?

Those answers may matter more than saving $20 a month on the premium.

Step 5: Record a Home Inventory Before You Need It

Insurance claims require proof. You may need to show what you owned, what condition it was in, and what was damaged. After a storm, memory is not a reliable filing system.

Use your phone to record a simple 5- to 10-minute video. Start outside: roof, siding, windows, yard, basement entry, mechanical systems. Then walk through each room and slowly capture furniture, electronics, appliances, tools, jewelry, cameras, musical instruments, and other major items. The goal is not beauty. The goal is evidence.

Upload the video to cloud storage and keep the date. For higher-value items, record serial numbers and receipts separately. If you run a small business from home and keep inventory, equipment, or work supplies there, document those separately because a personal homeowners policy may not fully cover business property.

Step 6: Give Medication and Pets Their Own Checklist

Household emergency planning often forgets medication and pets. Ready.gov's kit guidance includes supplies such as water, food, medicine, important documents, and other essentials for several days. For households with children, older adults, medical needs, or pets, this is not extra. It is core planning.

For medication, prepare:

- 3 to 7 days of essential prescriptions

- medication names, dosage, doctor, and pharmacy phone number

- health insurance cards and allergy information

- glasses, hearing aids, batteries, diabetes supplies, or other necessary devices

For pets, prepare:

- several days of food and water

- medication and vaccination records

- leash, carrier, litter, or cleaning supplies

- pet photo and microchip information

- hotels or shelters that accept pets

If pet bills and emergency care are part of your planning, these SmartLiving guides may help: Pet Emergency Vet Bill Red-Yellow-Green Guide and Is Pet Insurance Worth It?.

2026 Hurricane Season Household Money Checklist

- [ ] Check whether your homeowners policy excludes flood damage.

- [ ] Confirm whether you already have flood insurance and whether it could lapse.

- [ ] If considering an NFIP policy, understand the 30-day waiting period and exceptions.

- [ ] Save copies of homeowners, flood, auto, mortgage, and escrow documents.

- [ ] Keep $100 to $300 in small bills, not a large cash hoard.

- [ ] Confirm hurricane, wind, and normal deductibles.

- [ ] Record a home inventory video and upload it to cloud storage.

- [ ] Make a separate medication, medical information, and pet supply list.

- [ ] Prepare chargers, flashlights, water, basic food, and emergency contacts.

- [ ] Write down insurance claim phone numbers and app login steps on paper.

Final Takeaway

Hurricane preparation is not panic, and it is not buying a pile of things you will never use. It is clearing a few financial failure points in advance: which losses are not covered by standard homeowners insurance, which policy has a waiting period, how much deductible cash you need, where the claim documents are, and how you pay when the network is down.

If you have a mortgage, escrow account, homeowners insurance, and family responsibilities, hurricane season is a useful annual checkup. Do not wait until a storm watch appears to read the policy. In many cases, the most valuable preparation is the work you did 30 days earlier.

Disclaimer: This article is for general education and household financial-risk planning only. It is not insurance, legal, tax, disaster-safety, or personalized financial advice. Insurance terms, waiting periods, deductibles, flood risk, evacuation rules, and local emergency procedures vary by state, city, insurer, and property type. Confirm your situation with your insurance agent, lender, local emergency management office, or qualified professional before acting.

Related Financial Decisions

Keep using the same cash-flow lens on related decisions.

2026 PMI Cancellation Guide: When Can You Stop Paying Private Mortgage Insurance?

Private mortgage insurance is not always permanent. Use CFPB, Fannie Mae, Freddie Mac, and HUD rules to check 80% requests, 78% automatic termination, FHA MIP differences, and cash-flow math.

financeHomeowners Insurance Jumped in 2026? Audit Coverage Before Chasing the Cheapest Premium

A practical 2026 homeowners insurance audit for mortgage borrowers: escrow impact, deductibles, replacement cost vs. actual cash value, flood gaps, force-placed insurance, and cash-flow risk.

financeEscrow Shortage Added $275: Why a Fixed-Rate Mortgage Payment Rose in 2026

Why can a fixed-rate mortgage payment still rise? A practical 2026 CFPB-backed guide to escrow shortages, property tax, homeowners insurance, and a $600k payment example.

SmartLiving Tools

Keep running the numbers with free practical tools.