401(k) vs. Student Loan Payoff in 2026: What High-Income Borrowers Should Check First

High-income borrowers often turn this into a math contest.

Should I max out my 401(k), or pay off my student loans early?

It sounds like an investment question.

It is really a cash-flow question first.

You are not comparing one clean market return against one annoying loan balance.

You are comparing several different things at once:

Employer match.

Current tax rate.

Student loan interest rate.

Mortgage DTI.

Liquidity.

And the uncomfortable fact that money placed inside a retirement account is not the same as money sitting in a bank account.

So this guide is not trying to give one universal answer.

There is no universal answer.

A New York household earning $220,000 with a generous employer match and 4.5% student loans is not solving the same problem as a borrower earning $140,000 with no match, 8.94% Grad PLUS loans, and a home purchase planned within 12 months.

The useful move is to get the order right.

Step 1: Get the Employer Match Before Extra Student Loan Payments

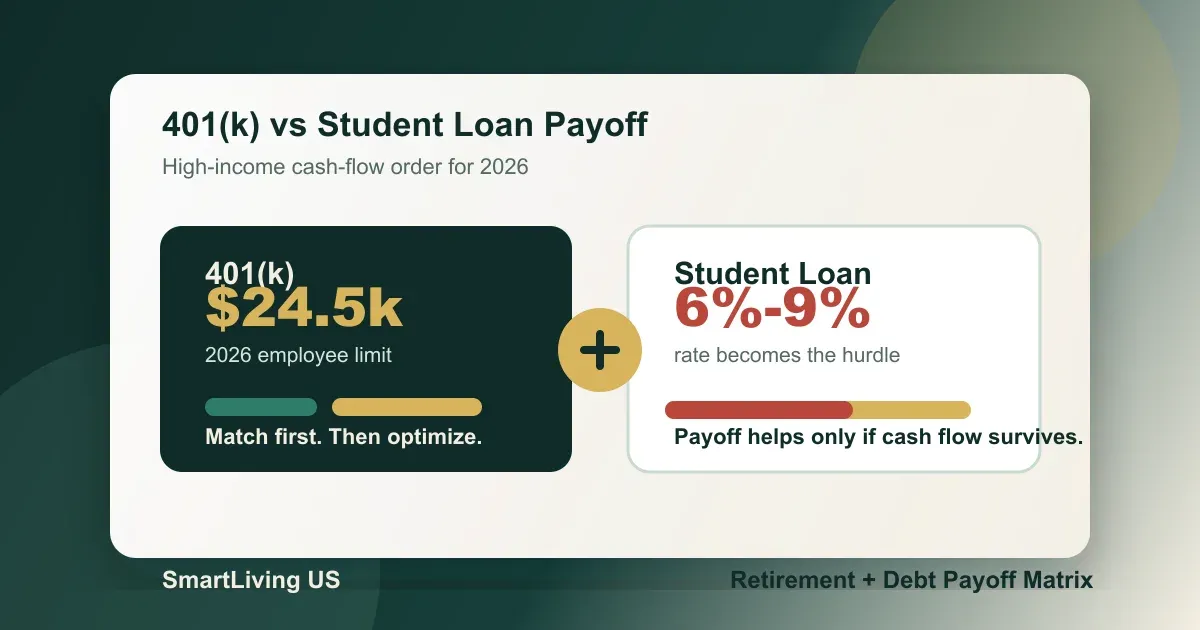

If your employer offers a 401(k) match, usually contribute enough to capture the match before making extra student loan payments.

The IRS describes employer matching contributions as employer contributions made when an employee makes elective deferrals, if the plan document permits. Source: IRS Retirement Topics: Contributions

That sounds technical.

In real life, it is compensation.

Assume your employer offers 100% match up to 4% of pay.

Your salary is $180,000.

You contribute 4%, or $7,200.

The employer contributes another $7,200.

If you skip that contribution because you want to pay extra on student loans, you are not just choosing debt payoff over investing.

You are leaving part of your compensation package unused.

That does not mean everyone should max out a 401(k).

But employer match should be separated from the rest of the decision. It is not the same as ordinary market return.

Use the 401(k) calculator to see how employee contributions and employer match compound separately. You can also read: 401(k) Employer Match: The Free Money Most People Underestimate.

Step 2: Know the 2026 401(k) Limits and Your Real Tax Bracket

For 2026, the basic 401(k) employee elective deferral limit is $24,500.

The IRS also lists a $8,000 catch-up contribution for many participants age 50 or older, a $11,250 higher catch-up limit for ages 60 through 63, and a $72,000 defined contribution limit. Source: IRS COLA increases for dollar limitations on benefits and contributions

Those limits matter.

But your marginal tax rate matters just as much.

Traditional 401(k) contributions may reduce current taxable income. Roth 401(k) contributions do not reduce current taxable income, but qualified distributions can be tax-free later.

For high-income earners in high-tax states or cities, the current-year tax effect of a traditional 401(k) contribution can be meaningful.

That is why the simple comparison, student loan at 6% vs. stock market at 7%, is too crude.

The actual comparison includes:

- Employer match

- Current tax deferral from traditional 401(k) contributions

- Future tax treatment of Roth 401(k) contributions

- Interest saved by paying down student loans

- Liquidity

- Mortgage DTI and home-buying plans

If you are still deciding between Roth and traditional, start here: Roth vs. Traditional 401(k) Guide.

Step 3: Treat the Student Loan Interest Rate as a Hurdle Rate

The higher the student loan rate, the harder it is to ignore early payoff.

The Department of Education’s Federal Register notice for fixed-rate Direct Loans first disbursed from July 1, 2025, through June 30, 2026 lists 6.39% for undergraduate Direct Subsidized and Unsubsidized loans, 7.94% for graduate and professional Direct Unsubsidized loans, and 8.94% for Direct PLUS loans. Source: Federal Register, Annual Notice of Interest Rates for Fixed-Rate Federal Student Loans

That does not mean your loans have those rates.

Your own loan details control.

Older federal loans may be lower.

Grad PLUS loans may be higher.

Private loans are a separate category.

But the range is a useful reminder.

Debt in the 6% to 9% zone is not a tiny background item.

Paying extra toward a 7.94% loan reduces a known interest cost.

But it is not the same thing as investment return.

Debt payoff reduces future interest and can lower financial stress.

The tradeoff is liquidity.

Once you send an extra $10,000 to a student loan, you usually cannot pull that money back out next month.

So higher rates make payoff more attractive.

But tighter cash flow makes full-speed payoff more dangerous.

Step 4: High Earners Should Not Overvalue the Student Loan Interest Deduction

Some borrowers say student loan interest is deductible, so there is no rush to pay it down.

For high-income borrowers, that argument is often weak.

IRS Topic 456 says the student loan interest deduction is limited to the lesser of $2,500 or the amount of interest actually paid during the year. It is gradually reduced and eventually eliminated as modified adjusted gross income reaches the annual limit for the filing status. Source: IRS Topic No. 456, Student Loan Interest Deduction

So do not assume the interest is meaningfully deductible.

Check whether you actually qualify.

Then compare after-tax costs.

Many high-income households face a student loan interest cost with little or no deduction, while 401(k) contributions may still have current tax value.

That makes the decision more nuanced.

It is not which one sounds more financially sophisticated.

It is which one helps your actual tax return and cash-flow table.

Step 5: If You Plan to Buy a Home, Think About DTI Before Paying Extra Principal

If you plan to buy a home within the next 12 to 24 months, the monthly student loan payment may matter more than the balance.

Mortgage lenders care about DTI, which compares monthly debt payments with gross monthly income. How the student loan payment is counted can affect mortgage room.

Extra principal payments do not always lower the required monthly payment.

Sometimes they shorten the repayment timeline.

Sometimes the servicer needs to recalculate the payment.

Sometimes the credit report does not immediately show the lower payment you expected.

So before sending a large extra payment, ask two questions.

First, will this extra principal payment reduce my required monthly payment?

Second, what monthly student loan payment will the mortgage underwriter use for DTI?

Otherwise you can end up with less cash but no meaningful improvement in the mortgage file.

Read the full breakdown here: Student Loans and Mortgage DTI in 2026. Then use the mortgage calculator to test the housing payment.

Step 6: Use a Practical Order Instead of a Perfect Answer

If you do not want to get trapped in an abstract 401(k) vs. student loan debate, use this order.

First, Keep a Cash Buffer

Do not drain the checking account to invest or pay down debt.

If one surprise expense sends you back to credit cards, the plan is too fragile.

Second, Capture the Employer Match

Contribute enough to get the full employer match if your plan offers one.

This does not mean 401(k) always beats debt payoff.

It means the match is part of compensation.

Third, Kill High-Interest Dangerous Debt First

If you have credit card debt near 20% and student loans near 6%, the credit card usually deserves attention first.

For a broader cash-flow order, read: Debt Payoff or Emergency Fund First?

Fourth, Compare Student Loan Rate With 401(k) Tax Value

If the student loan rate is 3% to 4%, and you have a strong match, high tax rate, and long retirement runway, 401(k) contributions may look more attractive.

If the student loan rate is 7% to 9%, there is no forgiveness path, and the interest deduction is not useful, extra payoff deserves serious consideration.

It does not have to be all or nothing.

Some households split extra cash.

For example, contribute enough for the match, then send extra payments toward the highest-rate student loan.

Or direct 70% of extra cash toward retirement and 30% toward loan payoff.

The split depends on the file.

Fifth, If You Are Buying a Home, Preserve Down Payment and DTI Flexibility

In New York especially, cash matters.

You may need down payment, closing costs, reserves, post-closing liquidity, and acceptable DTI.

Do not make the loan balance look prettier while weakening the cash position the mortgage file needs.

A Simple Example

Assume annual salary is $180,000.

The employer offers a 100% match up to 4%.

Student loan balance is $60,000 at an average 6.39%.

You have an extra $1,000 per month to allocate.

A practical order might look like this:

- Contribute at least 4% to the 401(k) to capture the match.

- If there is high-interest credit card debt, handle that first.

- If there is no high-interest credit card debt, decide whether the extra $1,000 should go entirely to student loans or be split between 401(k) contributions and loan payoff.

- If buying a home within a year, ask whether extra principal payments will actually improve the required monthly payment and DTI.

- If not buying soon, and the student loan rate is near 7% or higher, accelerating payoff on the highest-rate loan may strengthen the household balance sheet.

There is no magic answer.

But there is a useful principle.

Do not compare an average market return to your real loan, real tax bracket, real employer match, and real home-buying timeline.

Averages do not make your payments.

Cash flow does.

The Bottom Line

The 401(k) vs. student loan decision is not just about interest rate.

Use this order:

- [ ] Keep a basic cash buffer.

- [ ] Capture the full employer match.

- [ ] Pay down dangerous high-interest debt first.

- [ ] Check your actual student loan interest rates.

- [ ] Confirm whether the student loan interest deduction helps you.

- [ ] If buying a home, confirm whether extra payments improve DTI.

- [ ] Decide whether extra cash should go to 401(k), loan payoff, or both.

For high-income borrowers, the expensive mistake is not choosing A instead of B.

The expensive mistake is forcing every issue into one binary choice.

The real answer is usually an order of operations.

Take the money you should not leave behind.

Stop the most expensive leak.

Then optimize.

Sources

- IRS: Retirement Topics: Contributions

- IRS: COLA increases for dollar limitations on benefits and contributions

- Federal Register / Department of Education: Annual Notice of Interest Rates for Fixed-Rate Federal Student Loans

- IRS: Topic No. 456, Student Loan Interest Deduction

- Federal Student Aid: Top FAQs About Income-Driven Repayment Plans

Disclaimer: This article is for educational and informational purposes only. It is not investment, tax, legal, mortgage, or personal financial advice. 401(k) contributions, student loan repayment, IDR, refinancing, tax deductions, and mortgage DTI depend on your income, loan terms, employer plan, tax filing status, and lender rules. Before acting, consult your plan administrator, loan servicer, CPA, financial planner, or mortgage professional.

Related Financial Decisions

Keep using the same cash-flow lens on related decisions.

Student Loan Default in 2026: Wage Garnishment Is Delayed, But Default Still Matters

A practical 2026 guide to federal student loan default, delayed involuntary collections, wage garnishment, Treasury offsets, rehabilitation, consolidation, and cash-flow triage using ED, StudentAid.gov, and CFPB sources.

financeHELOC vs Cash-Out Refinance in 2026: Should You Tap Home Equity?

Home values are up, but home equity is not free cash. A 2026 guide to comparing HELOCs, home equity loans, and cash-out refinancing through payment shock, tax rules, and household cash flow.

financeStudent Loans and Mortgage DTI in 2026: What NYC Buyers Should Check Before Applying

Student loan debt does not automatically block a mortgage. The real issue is how the monthly student loan payment is counted in DTI. This guide uses CFPB, Fannie Mae, HUD/FHA, and StudentAid.gov sources to build a practical pre-approval checklist.

SmartLiving Tools

Keep running the numbers with free practical tools.