Thinking About Cashing Out Your 401(k)? Run the Tax and Penalty Math First

Most people do not think about cashing out a 401(k) because retirement is close.

They think about it because something changed.

A job ended.

A move is coming.

A home purchase suddenly needs cash.

Bills are tight.

The account shows $80,000, $120,000, or $200,000, and it feels like money sitting there waiting to be used.

That feeling is understandable.

It is also dangerous.

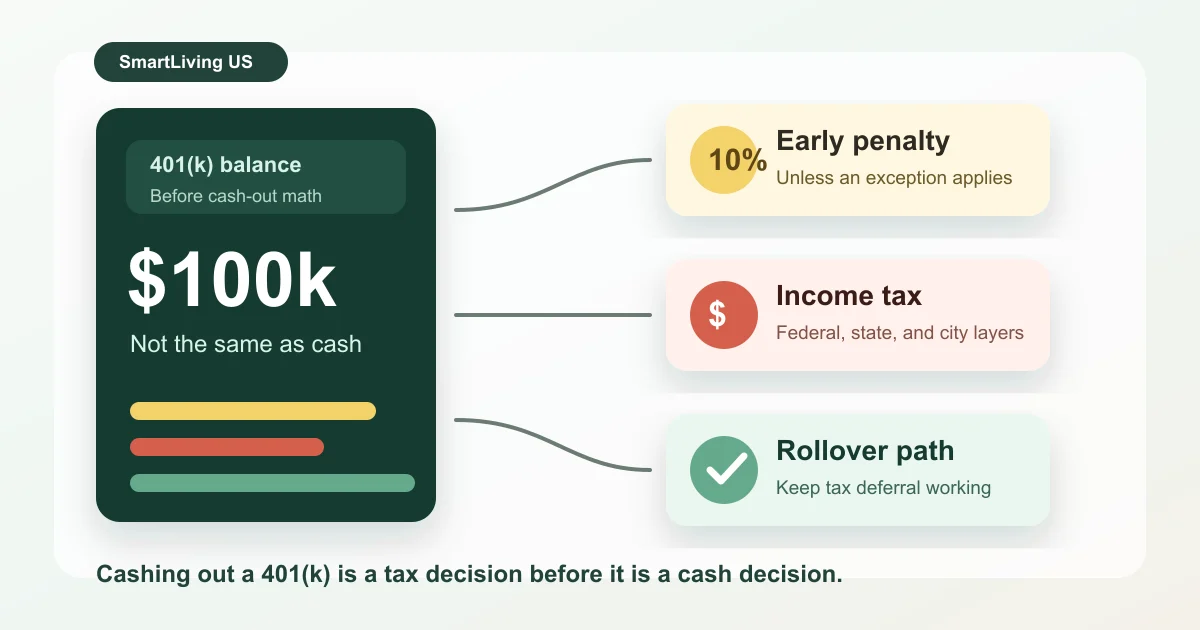

A 401(k) balance is not the same thing as spendable cash.

Especially with a Traditional 401(k), the money has usually been growing in a tax-deferred account. When you pull it out early, the tax system does not treat it like a regular savings account.

Before you hit the cash-out button, you need to answer three questions.

How old are you?

Does the distribution qualify for an exception?

Is the money being rolled over to another eligible retirement account?

If those questions are not clear, a cash-out can feel less like using your own money and more like taking apart a compounding machine for parts.

The First Layer Is the 10% Early Distribution Tax

The IRS says most retirement plan distributions are subject to income tax and may also be subject to an additional 10% tax. Generally, withdrawals from an IRA or retirement plan before age 59½ are early distributions, and the additional 10% tax applies unless an exception fits. Source: IRS early distribution exceptions

That is the part many people miss.

The 10% is not a replacement for regular income tax.

It is on top of it.

Here is a rough stress test.

Assume a 45-year-old New York resident takes $100,000 out of a Traditional 401(k), does not roll it over, and does not qualify for an exception.

| Item | Rough Amount | What It Means | | --- | ---: | --- | | Gross withdrawal | $100,000 | The number you see before taxes | | 10% early distribution additional tax | -$10,000 | Applies if no exception fits | | Federal income tax at an assumed 24% marginal rate | -$24,000 | Actual tax depends on full-year income | | State and city income tax stress test | -$8,000 to -$14,000 | Highly dependent on residency and tax facts | | Rough after-tax cash | About $52,000 to $58,000 | Not tax advice, just a planning warning |

This table is not a tax return.

It is a reality check.

The $100,000 account balance is not automatically $100,000 of usable cash.

If the withdrawal lands in the same year as wages, bonuses, short-term capital gains, unemployment benefits, or other taxable income, the result can change sharply.

That is why I do not like describing early 401(k) withdrawals as a simple emergency option.

They can be an emergency option.

But they are not a free one.

When You Leave a Job, Cashing Out Is Usually the Costliest Button

After leaving a job, your old 401(k) platform may show several choices.

Leave the money in the old plan.

Move it to the new employer plan.

Roll it over to an IRA.

Have the money paid to you.

The last option feels the simplest.

It can also be the most expensive.

The IRS explains that many pre-retirement payments from a retirement plan or IRA can be rolled over within 60 days, or transferred directly to another plan or IRA. A direct rollover generally has no tax withheld from the transfer amount. Source: IRS rollovers of retirement plan and IRA distributions

The tricky version is the indirect rollover.

If a retirement plan distribution is paid to you, the IRS says retirement plan distributions paid to you are generally subject to mandatory 20% withholding even if you intend to roll the money over later. If you later want to roll over the full amount, you need other cash to replace the withheld portion.

Here is the plain-English version.

You request $100,000 from an old 401(k).

The plan may withhold $20,000 and send you $80,000.

If you roll over only the $80,000 within 60 days, the missing $20,000 may become taxable income.

If you are under 59½ and no exception applies, that withheld portion may also face the 10% additional tax.

That is why a direct rollover can be cleaner than receiving the check personally.

The decision between an IRA and a new employer plan still matters. You may need to compare fees, investment choices, creditor protection, Roth versus Traditional balances, backdoor Roth IRA effects, and whether you might later need the age-55 separation exception.

But the first principle is simple.

If the goal is to keep retirement tax treatment intact, do not make cash-out the default.

Home Purchases and Hardship Withdrawals Are Easy to Misread

Home buying is one of the most misunderstood early-withdrawal topics.

You may have heard that first-time homebuyers can get a $10,000 exception.

That is not a blanket 401(k) rule.

The IRS early-distribution exception table lists qualified first-time homebuyer distributions up to $10,000 as available for IRAs, but not for qualified plans such as 401(k)s.

So do not casually apply an IRA homebuyer rule to your 401(k).

If you are considering using retirement money for a down payment, read your plan document and talk with the plan administrator and a tax professional first.

Hardship withdrawals also need careful wording.

The IRS defines a hardship distribution as a withdrawal from a participant's elective deferral account because of an immediate and heavy financial need, limited to the amount necessary to satisfy that need. The money is taxed to the participant and is not paid back to the account. Source: IRS hardships, early withdrawals and loans

That means a hardship withdrawal may be allowed by the plan.

It does not mean every hardship withdrawal automatically avoids the 10% additional tax.

Some exceptions exist, such as certain medical expenses, qualified birth or adoption distributions, qualified disaster distributions, certain emergency personal expenses, domestic abuse victim distributions, and separation from service during or after the year you reach age 55.

But each exception has its own conditions.

The right questions are:

Does the plan allow this distribution?

Is the distribution taxable?

Does it meet a specific 10% additional-tax exception?

Those are three different questions.

Do not let one yes answer stand in for all three.

A 401(k) Loan Can Be Gentler, but It Is Not Free Money

If your plan allows it, a 401(k) loan may be less harsh than a withdrawal.

The IRS says retirement plans may offer participant loans, but plan sponsors are not required to include loan provisions. For plans that allow loans, the maximum loan amount is generally 50% of the vested account balance or $50,000, whichever is less. Source: IRS retirement topics, plan loans

The upside is that a compliant loan repaid on schedule usually is not immediately treated as taxable income.

But there are two real costs.

First, the borrowed money is no longer following the original investment path inside the account.

Second, job changes can make the loan riskier. The IRS notes that plan sponsors may require repayment of the full outstanding balance if employment ends. If the employee cannot repay it, the employer treats the balance as a distribution and reports it on Form 1099-R. Loans that fail to meet repayment rules may also become deemed distributions subject to income tax and possibly the 10% early distribution tax.

So a 401(k) loan is not evil.

It is also not painless.

It is a way of borrowing against future retirement money to solve a current cash problem.

That can be reasonable.

But it should be deliberate.

Build Two Tables Before You Touch the Account

If you are thinking about pulling from a 401(k), do not start with the question, "Can I access the money?"

Start with two tables.

The first table is today's cash.

| Question | What to Check | | --- | --- | | Does the plan allow withdrawal, loan, or rollover? | Read the Summary Plan Description | | Gross withdrawal amount | Example: $100,000 | | Are you under age 59½? | This determines early-distribution exposure | | Does a specific exception apply? | Check the IRS exception table | | Federal marginal tax rate | Estimate based on full-year taxable income | | State and city tax | Based on where you are resident when income is recognized | | Is 20% withholding required? | Especially if paid directly to you | | Estimated usable cash | Do not confuse balance with cash |

The second table is the money if you leave it alone.

That table is less emotional because it is not today's cash.

But it is the heart of 401(k) planning.

Open the SmartLiving 2026 401(k) calculator. Enter your age, retirement age, salary, current balance, contribution rate, employer match, expected return, and inflation assumption.

Then compare.

If that $100,000 remains invested until age 65, what might it become?

What is the inflation-adjusted value?

Using a 4% withdrawal assumption, how much annual retirement income might it support?

If you turn on the New York tax-drag estimate, what does the annual withdrawal look like after the local-tax stress test?

The calculator is not an early-withdrawal tax calculator.

It will not fill out Form 5329.

It will not decide whether you qualify for an IRS exception.

Its job is to show the other side of the trade.

The cost of cashing out is not only the tax and penalty today.

It is also the future compounding you give up.

My Rule of Thumb: Treat the 401(k) as a Last Door, Not the First Drawer

Not everyone can avoid touching retirement money.

Life is not a spreadsheet.

Job loss, medical bills, family obligations, relocation, immigration changes, and home purchases can all create real pressure.

But the more serious the pressure, the more important it is to avoid sloppy math.

Before you cash out, ask at least five questions.

| Question | Why It Matters | | --- | --- | | Am I under age 59½? | Determines early-distribution risk | | Do I qualify for a 10% exception? | Hardship is not automatically penalty-free | | Can I do a direct rollover instead? | May avoid withholding and 60-day rollover stress | | Is a loan safer than a withdrawal? | Only if repayment and job-risk assumptions hold | | What would the money become if left invested? | This is the opportunity cost |

A 401(k) is not untouchable.

But it should usually be a last door, not the first drawer.

The smart move is not "never touch it."

The smart move is to put the taxes, penalty, withholding, rollover mechanics, loan risk, and lost compounding on the table before you decide.

If you still need to use it after running the numbers, at least it is a conscious decision.

Not a decision made because the balance looked like cash.

If you are still in the contribution stage, these two related guides can help you plan the front half of the equation:

- How Much Should You Put in Your 401(k) in 2026? Use a Calculator Before Guessing

- How Much Is Your 401(k) Employer Match Really Worth?

Disclaimer: This article is for educational and informational purposes only. It is not investment, tax, legal, or personal financial advice. 401(k) distributions, rollovers, hardship withdrawals, loans, withholding, 10% additional-tax exceptions, state tax, and city tax can depend on age, account type, plan documents, separation timing, residency, filing status, annual income, and future law changes. Before taking a distribution, rollover, or loan, consult your plan administrator, CPA, tax adviser, attorney, or qualified financial professional.

Related Financial Decisions

Keep using the same cash-flow lens on related decisions.

How Much Should You Put in Your 401(k) in 2026? Use a Calculator Before Guessing

A practical 2026 guide to choosing a 401(k) contribution rate using IRS limits, employer match, inflation-adjusted purchasing power, and a realistic New York withdrawal-tax estimate.

financeRoth 401(k) vs. Traditional 401(k) in 2026: A Practical Tax-Now or Tax-Later Guide

Choosing Roth or Traditional 401(k) is not about which account earns more. It is about when you pay taxes. Use 2026 IRS limits, tax brackets, employer match, state taxes, and cash flow to make a clearer decision.

financeSolo 401(k) vs SEP IRA in 2026: Which Retirement Plan Fits a One-Person Business?

A practical 2026 guide for freelancers, consultants, Shopify sellers, and one-person businesses comparing Solo 401(k) and SEP IRA contribution room, Backdoor Roth issues, Form 5500-EZ, and admin cost.

SmartLiving Tools

Keep running the numbers with free practical tools.