Student Loan Default in 2026: Wage Garnishment Is Delayed, But Default Still Matters

One of the easiest student loan headlines to misread in 2026 is this one: wage garnishment is delayed.

That sounds like relief.

And for many borrowers, it is.

If rent, insurance, car payments, credit card minimums, and grocery bills already consume most of your paycheck, a delay in federal student loan wage garnishment can feel like someone finally opened a window.

But delayed collection is not the same thing as erased debt.

It is not the same thing as forgiveness.

And it does not automatically move a federal student loan out of default.

This guide is about federal student loans only. Private student loans follow different rules, different collection paths, and different legal risks.

Let’s pin down the 2026 policy backdrop first.

On January 16, 2026, the U.S. Department of Education announced that it would delay involuntary collections on federal student loans, including Administrative Wage Garnishment, or AWG, and the Treasury Offset Program, or TOP. The Department described the delay as temporary and tied it to repayment reforms that could give defaulted borrowers more time to evaluate repayment options, consolidate loans, or begin rehabilitation. Source: U.S. Department of Education, Delays Involuntary Collections.

The important word is not just delay.

It is temporary.

Then, on March 19, 2026, the Department of Education and the Treasury Department announced a Federal Student Assistance Partnership that includes work around returning defaulted borrowers to repayment. Source: ED and Treasury Announce Federal Student Assistance Partnership.

So the practical reading is simple.

The collection machine may be slowing down.

It has not disappeared.

If your federal student loan is already in default, the useful question is not whether your paycheck is being garnished today.

The useful question is whether you can use this window to get the loan out of default before the system hardens again.

Default Is Not Just a Late Payment

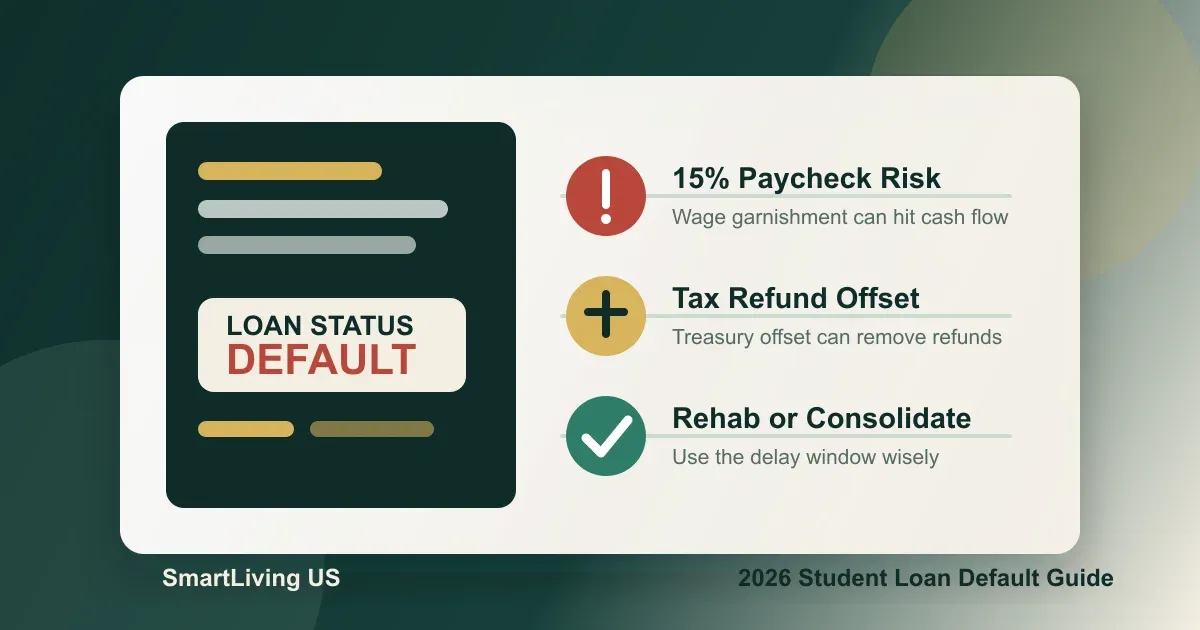

Federal Student Aid says that if you do not make scheduled payments for at least 270 days, your federal student loan goes into default. If you have not made a payment for more than 360 days and do not take action, involuntary collections may begin. Those methods can include wage garnishment, where up to 15% of your paycheck may be withheld, and Treasury offset, where federal tax refunds or other federal benefits may be withheld. Source: Student Loan Default and Collections: FAQs.

That is why default is different from being a few days late.

It can hit several parts of your financial life at once.

First, cash flow.

If AWG starts, the government is no longer waiting for you to decide how much you can pay that month. A portion of disposable pay can be withheld before the money reaches your budget.

Second, refunds and benefits.

Treasury offset can affect a federal tax refund or certain federal payments. For many households, a tax refund is the largest cash cushion of the year. Losing it can push other balances right back onto credit cards.

Third, credit.

The Department of Education also notes that defaults are reported to credit reporting agencies and may harm credit reports.

Fourth, future options.

Default can block access to deferment, forbearance, income-driven repayment plans, and additional federal student aid until the default is resolved.

That is why the 2026 delay should not be treated like a free pass.

It is more like a planning window.

Do These Five Things Before Chasing a Miracle Fix

If you think your federal student loan may be in default, do not start with social media advice or debt relief ads.

Start with the official trail.

Step 1: Check Whether You Are in Default Right Now

Log in to StudentAid.gov and open My Aid to confirm whether any federal student loan is marked in default.

Federal Student Aid says that borrowers with a federal student loan in default should see a warning message on the StudentAid.gov dashboard, and loan details can confirm the status of each loan.

Step 2: Update Your Mailing Address Before Notices Go Missing

Update your mailing address so default, repayment, AWG, or Treasury offset notices do not go to an old address.

Default notices and repayment documents may arrive by mail. If your address is old, you can miss a response window without realizing it.

Step 3: Use MyEdDebt.ed.gov If Your Loan Moved to DRG

If your defaulted federal loan has been transferred to the Default Resolution Group, create a MyEdDebt.ed.gov account and review the debt status there.

MyEdDebt.ed.gov is the official Department of Education site for borrowers with defaulted federal student loans. Federal Student Aid explains that if your loan is transferred to DRG, you need to create a separate MyEdDebt account. Your StudentAid.gov username and password will not work there. Official portal: MyEdDebt.ed.gov.

Step 4: Look for Treasury Offset or Wage Garnishment Status

Check whether your account shows Treasury Offset Program or Administrative Wage Garnishment status before assuming the delay protects you.

StudentAid.gov says MyEdDebt may show status messages such as Certified for TOP or Account is in AWG. Even during a delay, you should know where your account sits.

Step 5: Build a 30-Day Cash-Flow List Before Choosing a Fix

List the next 30 days of required expenses before choosing rehabilitation, consolidation, or another default-resolution path.

Write down rent, food, utilities, insurance, transportation, credit card minimums, and any required loan payments. Then look at what you can realistically use to resolve the default.

2026 Student Loan Default Triage Checklist

- [ ] Check your federal loan status on StudentAid.gov.

- [ ] Update your mailing address and contact information.

- [ ] Create a MyEdDebt.ed.gov account if your loan is with DRG.

- [ ] Look for TOP, AWG, or other collection-status messages.

- [ ] Write down 30 days of essential expenses and minimum payments.

- [ ] Compare rehabilitation and consolidation before signing paperwork.

- [ ] Save copies of notices, payment confirmations, and agreement letters.

If the basics are already tight, read this first: Debt Payoff or Emergency Fund First? A 2026 Cash-Flow Order.

Do not build a plan from panic.

Build it from cash flow.

Rehabilitation vs. Consolidation

For defaulted federal student loans, the two common exit routes are loan rehabilitation and loan consolidation.

They can both move a loan out of default, but they do not work the same way.

| Option | Best fit | Main advantage | Main tradeoff | | :--- | :--- | :--- | :--- | | Loan rehabilitation | Borrowers who can follow a payment agreement and want the best shot at repairing the default record | Federal Student Aid says rehabilitation can remove the record of the defaulted loan from credit history | Slower, requires a rehabilitation agreement and several on-time payments | | Direct consolidation | Borrowers who need a faster route out of default and back into repayment options | Federal Student Aid describes consolidation as faster than rehabilitation | The default record can remain on credit history, and collection costs or capitalized interest may increase total debt | | Repayment in full | Borrowers with enough cash to clear the debt | Fastest resolution | Unrealistic for many households |

Federal Student Aid’s rehabilitation FAQ includes a key payment formula. Under a standard rehabilitation agreement, the monthly payment is generally 15% of annual discretionary income divided by 12. If that amount is not affordable, borrowers may be able to submit a Loan Rehabilitation Income and Expense form to request an alternative payment based on current financial circumstances. Source: Student Loan Rehabilitation for Borrowers in Default: FAQs.

This is why the cash-flow step matters.

Rehabilitation may look better on paper if your priority is cleaning up the default record.

But if the payment agreement is not sustainable, the plan can break.

Consolidation may be faster, but you need to accept the credit-history and cost tradeoffs.

There is no perfect option.

There is only the option you can actually complete.

Be Careful With Third-Party Debt Relief Pitches

Student loan stress creates a perfect market for aggressive promises.

Be especially careful with phrases that promise an immediate default deletion, a fast approval shortcut, or a result that sounds too clean for a messy federal loan file.

The CFPB provides a consumer hub for student loan borrowers and repayment options here: CFPB Student Loans.

My own rule of thumb is blunt.

If a company asks for a large upfront fee, promises to erase a federal student loan default immediately, or tells you not to contact StudentAid.gov, your servicer, DRG, or a guaranty agency, slow down.

The core official paths for federal student loan default should run through StudentAid.gov, your loan servicer, MyEdDebt.ed.gov, DRG, or the relevant FFEL guaranty agency.

Do not hand your most sensitive financial information to a page that only knows how to scare you.

If Money Is Tight, Use This Priority Order

The least useful advice is to simply say: make your payments and protect your credit.

That is true.

It is also not enough.

Many borrowers are not ignoring their loans because they enjoy the stress. They are trying to survive a tight monthly cash-flow equation.

So the order should be realistic.

First, protect rent, food, basic medical needs, necessary transportation, utilities, and insurance.

Second, protect minimum payments and bills that can trigger immediate damage, especially rent-related obligations, credit cards, and auto loans.

Third, confirm the student loan status and contact the servicer, DRG, or guaranty agency to choose rehabilitation or consolidation.

Fourth, stop small leaks.

Subscriptions, buy now pay later balances, automatic renewals, and installment plans can quietly drain the money you need for the default plan. These two guides can help: Subscription Bill Audit and BNPL Hidden Costs.

Fifth, once the loan is out of default, then think about accelerating payoff, rebuilding savings, investing, and retirement contributions.

The order matters.

If the order is wrong, you can work hard and still feel like the system keeps pulling blood from your cash flow.

The Real Point

The 2026 student loan default story is not about predicting every policy change.

You cannot control the policy calendar.

You can control three things.

Confirm the account status.

Choose an official path.

Use the delay to move the loan out of default before involuntary collections become a harder problem again.

If you see a headline saying wage garnishment is delayed, the best response is not to forget the loan.

It is to log in and check your account.

That might feel uncomfortable.

But it is cheaper than discovering the problem when a paycheck or tax refund is already missing.

Sources

- U.S. Department of Education: Delays Involuntary Collections Amid Ongoing Student Loan Repayment Improvements

- U.S. Department of Education: Federal Student Assistance Partnership with Treasury

- Federal Student Aid: Student Loan Default and Collections: FAQs

- Federal Student Aid: Student Loan Rehabilitation for Borrowers in Default: FAQs

- CFPB: Student Loans

Disclaimer: This article is for educational and informational purposes only. It is not legal, tax, investment, or personal financial advice. Student loan rules, repayment options, collection timelines, and borrower eligibility can change. Before acting on a defaulted student loan, check current instructions from StudentAid.gov, MyEdDebt.ed.gov, your loan servicer, DRG, a guaranty agency, or a qualified professional.

Related Financial Decisions

Keep using the same cash-flow lens on related decisions.

401(k) vs. Student Loan Payoff in 2026: What High-Income Borrowers Should Check First

Should high-income borrowers max out a 401(k) or pay off 6% to 8% student loans early? This guide uses IRS 2026 contribution limits, Federal Register student loan rates, and StudentAid.gov sources to compare employer match, taxes, cash flow, DTI, and payoff order.

financeStudent Loans and Mortgage DTI in 2026: What NYC Buyers Should Check Before Applying

Student loan debt does not automatically block a mortgage. The real issue is how the monthly student loan payment is counted in DTI. This guide uses CFPB, Fannie Mae, HUD/FHA, and StudentAid.gov sources to build a practical pre-approval checklist.

financeHELOC vs Cash-Out Refinance in 2026: Should You Tap Home Equity?

Home values are up, but home equity is not free cash. A 2026 guide to comparing HELOCs, home equity loans, and cash-out refinancing through payment shock, tax rules, and household cash flow.

SmartLiving Tools

Keep running the numbers with free practical tools.